Crypto HNWIs: who they are and how they made their wealth

Over the past decade, cryptocurrencies have evolved from a fringe experiment into a significant driver of global wealth creation. For banks, this shift presents both an opportunity and a challenge: how to responsibly onboard and serve crypto high net worth individuals (HNWIs) while meeting regulatory and compliance (and reputational) requirements.

Focus on Millennials & Gen-Z

Crypto adoption has grown rapidly. As of 2024, approximately 560 million people globally own or have owned cryptocurrency, with adoption heavily skewed toward younger generations. Around 40% of millennials report holding crypto, compared to just 4% of baby boomers, and over half of Gen-Z investors in the US and UK have held crypto at some point. In 2025, there were an estimated 145,000 Bitcoin millionaires and over 240,000 crypto millionaires worldwide.

These individuals tend to be tech-savvy, globally mobile, and digitally native. Typically, a significant portion of their net worth is in crypto, with Bitcoin and Ethereum forming the core of most portfolios. Notably, few have had significant interaction with traditional financial institutions such as private banks and wealth managers.

How Was Crypto Wealth Created?

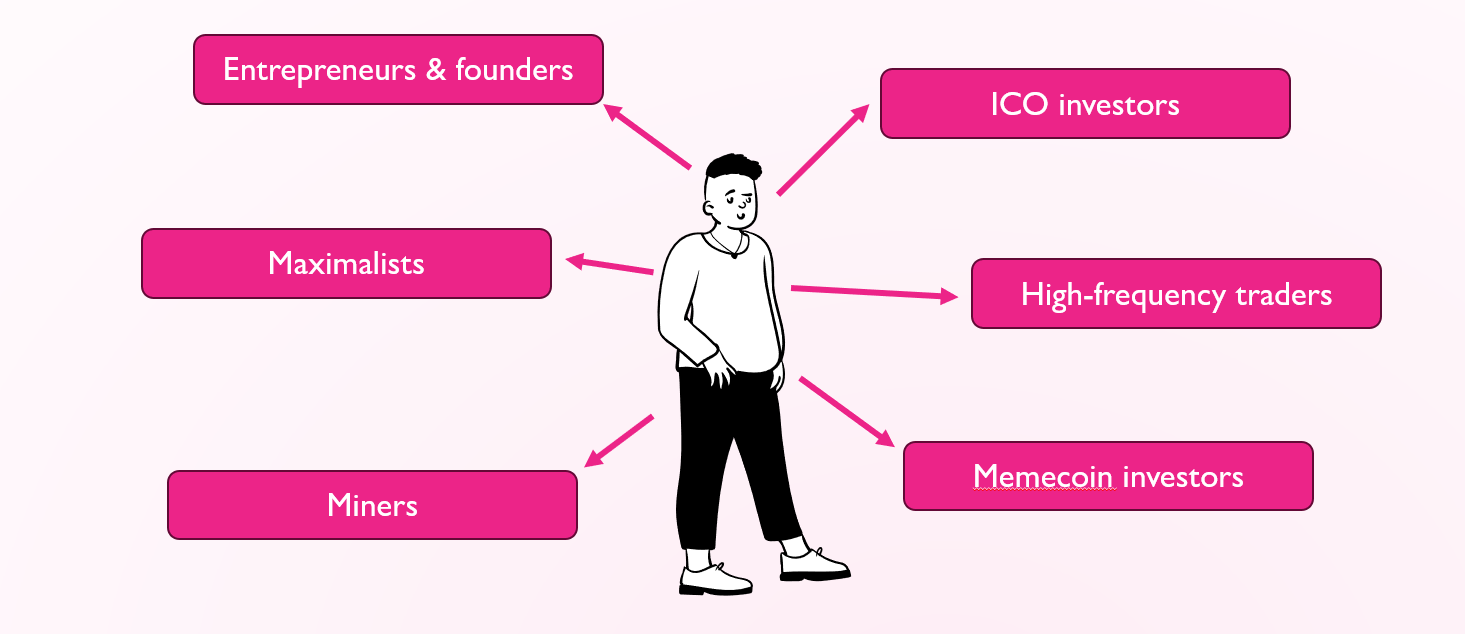

Understanding the origin of wealth is essential for both relationship management and compliance. In the main, crypto wealth has emerged through five distinct waves. This started in 2010 with the early Bitcoin adopters - hobbyist and enthusiasts - and moved on to Ethereum ICO investors in 2015 (which involved around 8,000 investing wallets). A large portion of this cohort are now UHNWIs, having acquired ETH at around $0.25 per coin.

In 2017, the ICO craze saw a proliferation of tokens and the third wave of wealth creation. A two-year bear market was broken in 2021 with the rise of decentralised finance - and to a lesser extent NFTs. DeFi saw huge capital inflows into the market and the creation of a swathe of new crypto builders from everything to exchange platforms to lending and borrowing services. This caused BTC to move from under $10,000 per token to over $50,000.

Notably, many of the entrepreneurs from this period had token lock-ins or vesting schedules that ended in 2023 or 2024. Whilst many sought to move these funds to traditional finance, others were used to participate in the fifth and final wave - that of memecoins.

In a 12 month period from early 2024, Solana led a massive bull run, with the native token increasing by over 1,000 percent, with far bigger increases in other tokens. For example, during a three-month period in late 2024, Fartcoin, a popular memecoin, experienced price increases of over 4 million percent.

These assets often have no intrinsic value, formal business model, or cash flows. Instead, they are driven by speculative momentum, online communities, influencers, and rapid retail participation. But key to this wave was the ease with which participants could create, launch and trade tokens through platforms like Pump.Fun. This democratisation drove retail participation, with billions of dollars flowing into Solana.

However, this phase created wider issues when assessing wealth making journeys. One of the challenges when onboarding crypto HNWIs is not the existenceof crypto wealth, but the speed at which that wealth can be created. Traditional wealth accumulation - through entrepreneurship, property, or capital markets - typically unfolds over years or decades. In crypto markets, by contrast, material wealth can be generated in weeks or even days, creating tension with conventional source-of-wealth expectations.

Many crypto protocols provide direct programmatic access to order books and on-chain data. This allows traders to deploy algorithms that can execute thousands of trades per second, respond instantly to price movements, and exploit small inefficiencies across markets. Bot traders and high-frequency traders (HFTs) have emerged in crypto as a natural consequence of this effect - none more so than the2024 Solana bull run which saw an influx of algorithmic and bot traders.

For relationship managers, the challenge is often communicative rather than technical. Crypto HNWIs may struggle to explain their wealth trajectory in ways that align with bank onboarding frameworks. A client whose net worth increased 100x in a matter of weeks may appear evasive or implausible when, in reality, their experience reflects normal - if extreme - market dynamics within crypto ecosystems.

The Evolving Crypto Risk Landscape

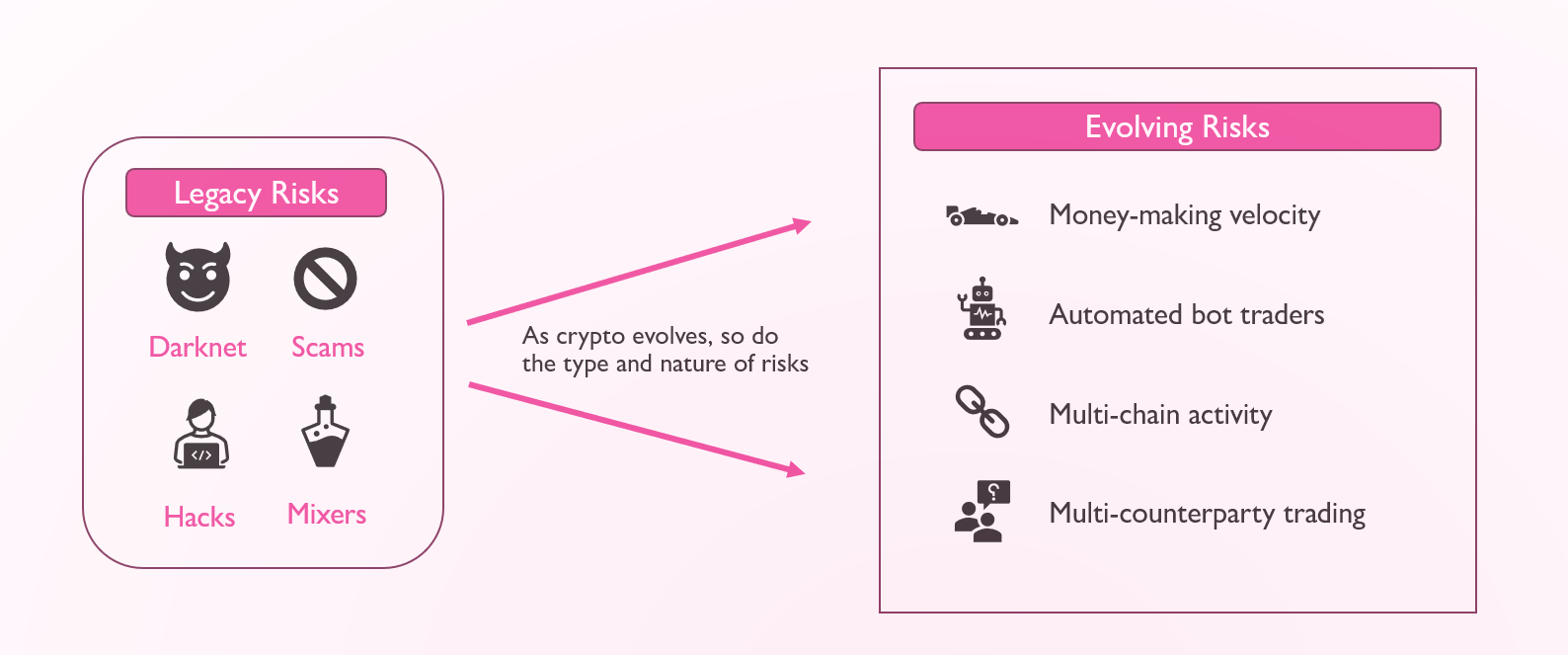

As crypto markets mature and wealth creation diversifies, risk is shifting away from purely illicit activity toward structural and behavioural risks that challenge traditional compliance frameworks. These evolving risks do not necessarily indicate higher levels of criminal activity. Instead, they reflect:

- Faster capital movement

- Greater technical sophistication

- More decentralised market participation

As crypto evolves, risk assessment must evolve with it. Effective compliance increasingly relies on contextual understanding of on-chain behaviour, transaction patterns, and market events - using blockchain data as a transparency tool rather than treating complexity itself as a red flag.

And because of these issues, crypto investors often approach banks with caution. There is anxiety around explaining highly technical or unconventional wealth-creation journeys to non-specialists. And some rightly fear debanking or being classified as high-risk simply due to their asset class.

Yet, despite this suspicion, crypto HNWIs do need banks. Common motivations include diversification; legitimising their wealth by converting crypto into fiat; and long-term wealth protection, particularly for estate and succession planning. In our experience, education and empathy are critical. Most crypto HNWIs have never worked with private banks before, so RMs should prioritise understanding their background rather than forcing them into traditional templates.

Key engagement principles include:

- Get their story: Crypto investors are often passionate about their journey and willing to explain it if approached respectfully.

- Understand the mechanics: Ask about key investments, counterparties, exchanges, wallets, and withdrawal methods.

- Know what to ask for: Clear, well-explained documentation requests build trust and reduce friction (think: wallets, statements, agreements, etc).

- Address data security head-on: Be transparent about how client data is used, stored, and protected.

Crypto HNWIs represent a growing and increasingly important client segment for banks. While their profiles and wealth origins may differ from traditional clients, their underlying needs - stability, legitimacy, and long-term planning - are familiar. Relationship managers who take heed of this will be best positioned to build durable, profitable relationships in this emerging area.

Onboarding Crypto HNWIs: The Complete Guide

Hoptrail partners with Weatherbys Bank

Hoptrail 2.0

Subscribe to the Hoptrail newsletter

Sign up with your email address to get the latest insights from our crypto experts.